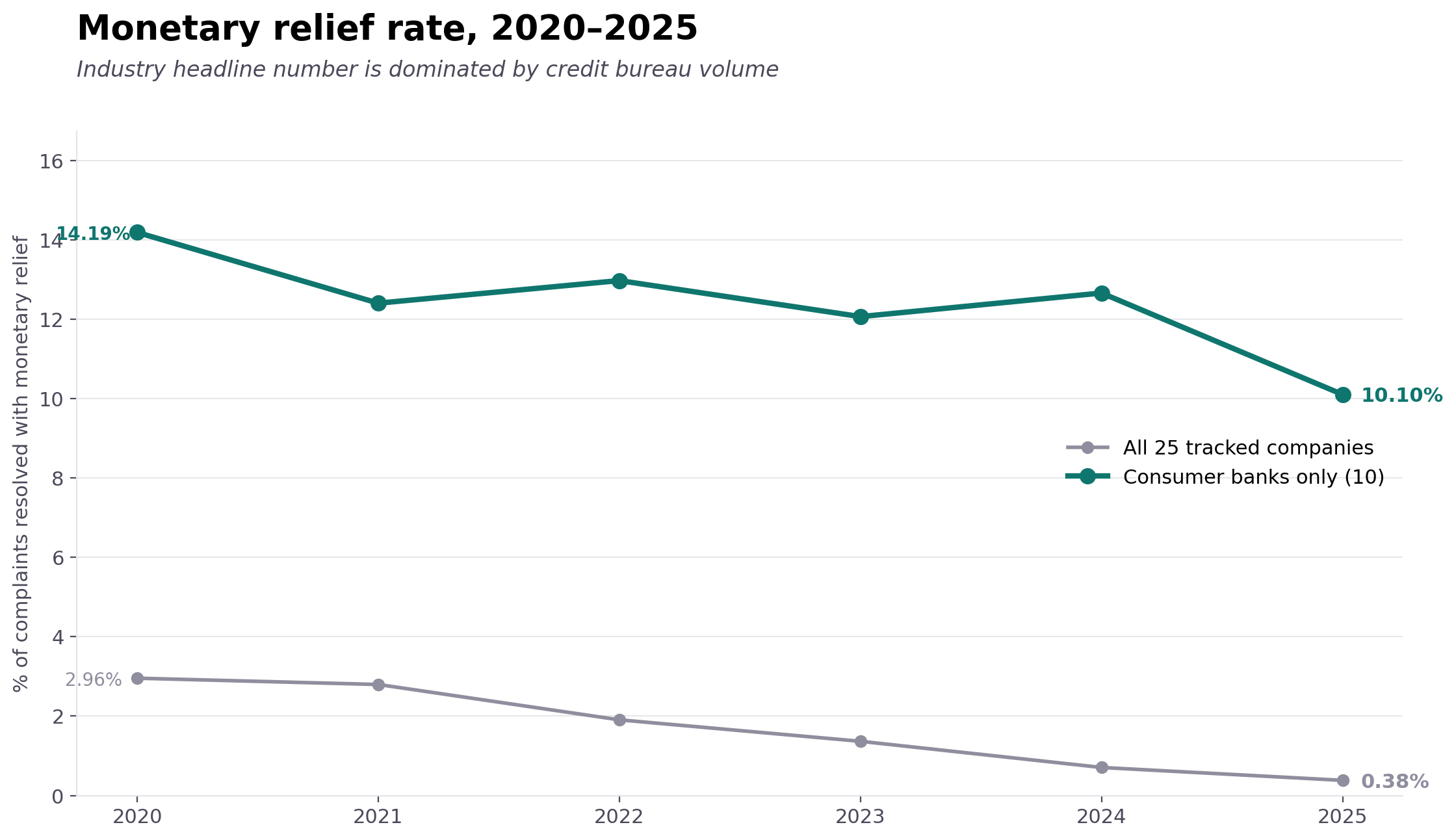

The industry-wide monetary-relief rate (all 25 companies) fell from 2.96% in 2020 to 0.38% in 2025. The same metric calculated only across the 10 tracked consumer banks fell from 14.19% to 10.10%. The divergence reflects the composition of the dataset: roughly 80% of total complaints since 2020 were filed against the three major credit bureaus, where complaints are processed under FCRA rules that rarely involve monetary relief as a resolution type.

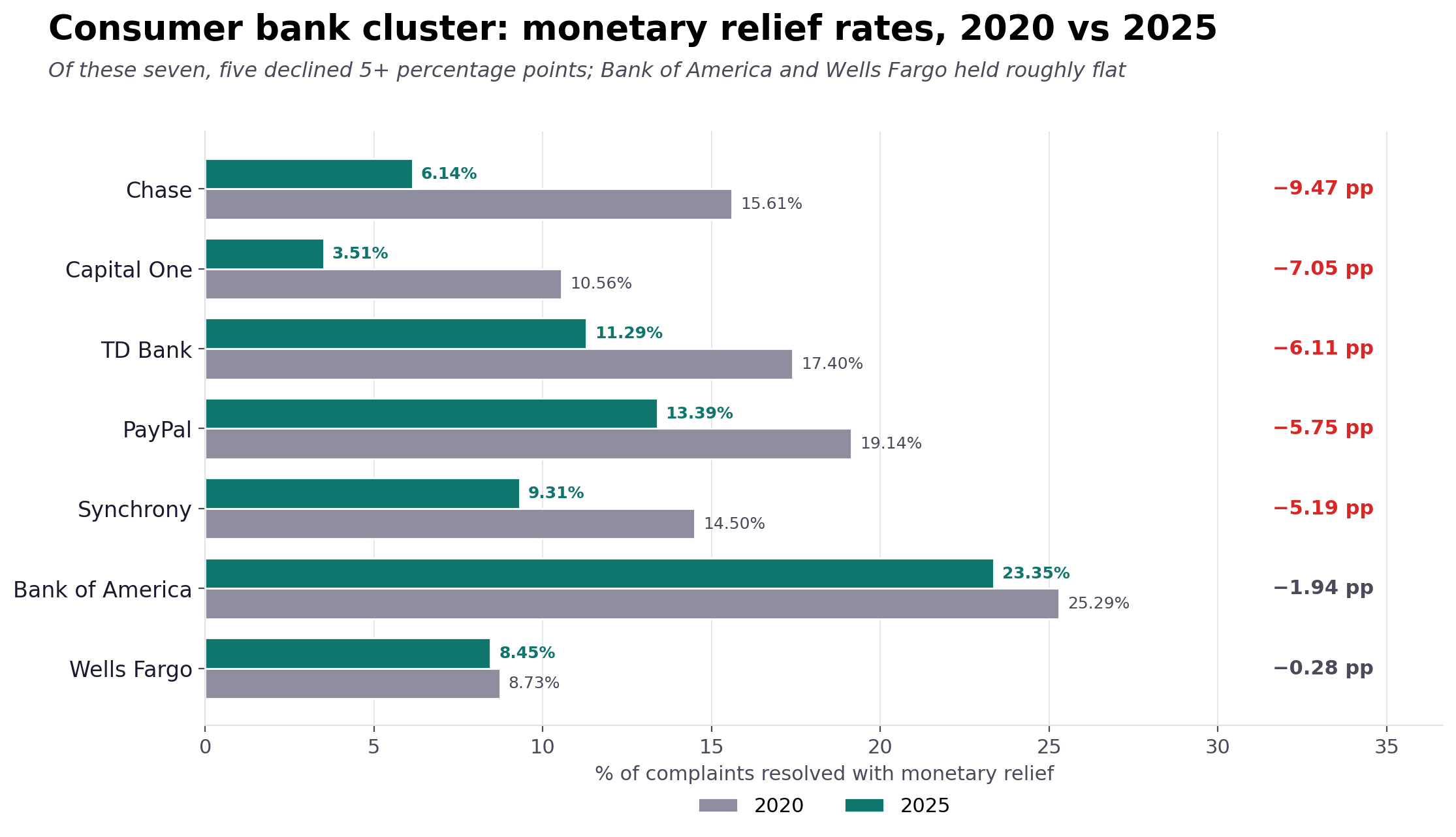

Monetary-relief rates for seven major consumer banks, 2020 vs 2025. Chase declined 9.47 percentage points, the largest drop in the cluster. Four additional companies — Capital One, TD Bank, PayPal, Synchrony — declined between 5.19 and 7.05 points. Bank of America and Wells Fargo declined under 2 points. Citibank is not shown in this chart; its rate rose 4.11 points over the same window and appears in the full table below.

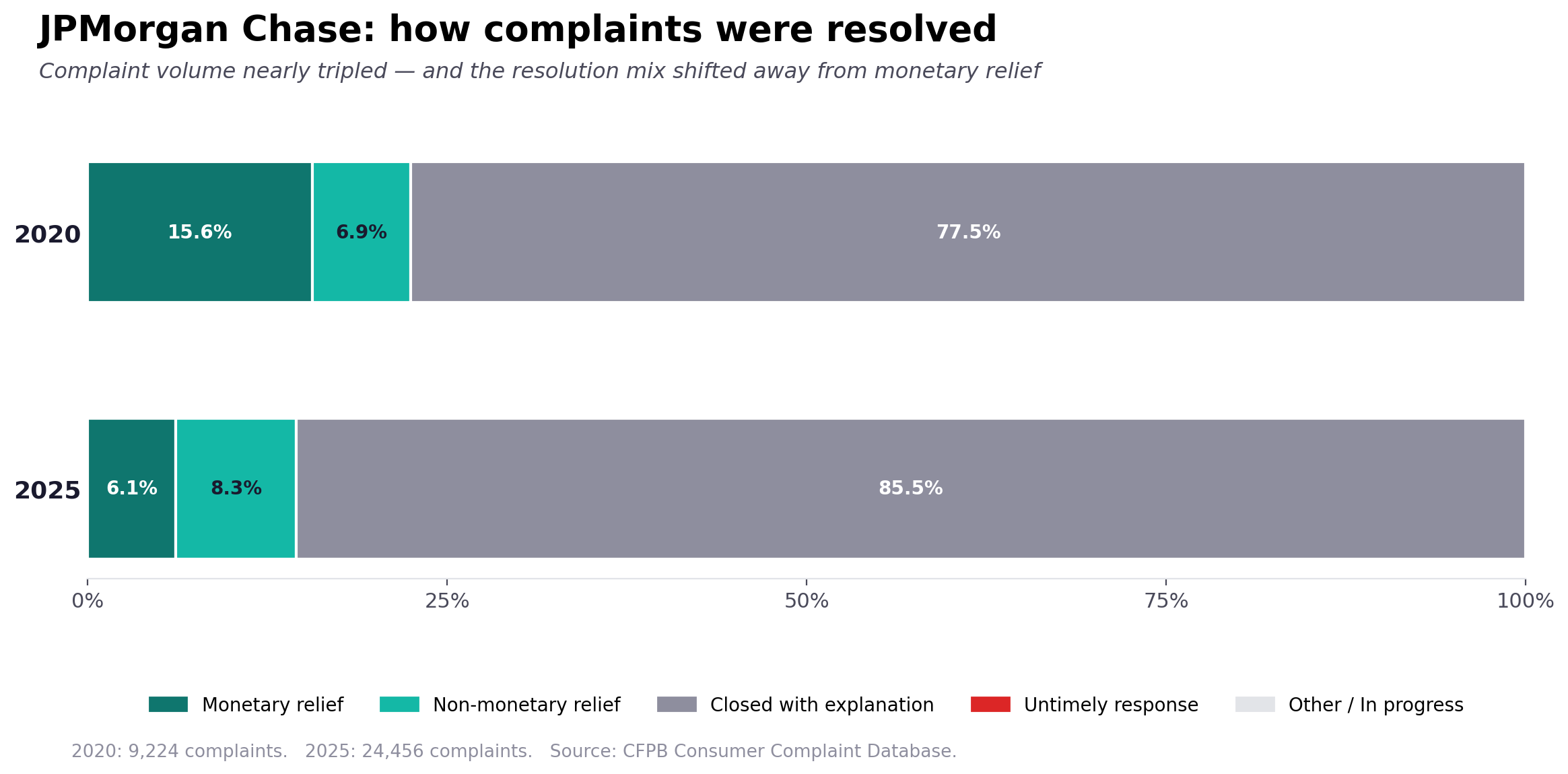

Composition of Chase's complaint resolutions in 2020 and 2025. Complaint volume grew from 9,224 to 24,456 (a 2.65× increase). The monetary-relief share fell from 15.6% to 6.1%. The non-monetary relief share rose from 6.9% to 8.3%. The "closed with explanation" share — resolutions where the company provided a written response but no relief — rose from 77.5% to 85.5%.

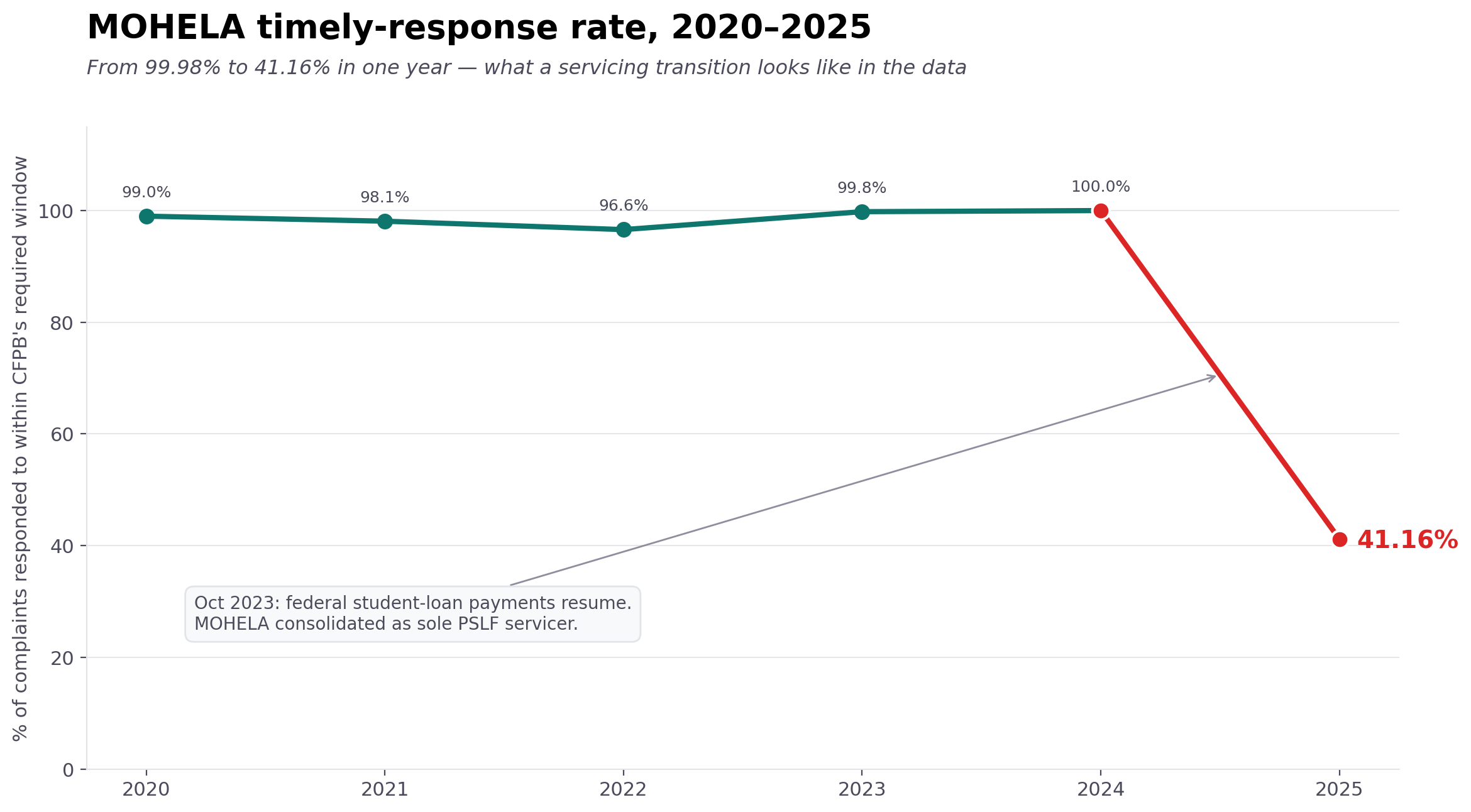

MOHELA's annual timely-response rate, 2020–2025. Rates held between 96.57% and 99.98% through 2024. In 2025 the rate dropped to 41.16%, a 58.82-point decline year-over-year. The 2025 drop coincides with the full resumption of federal student-loan servicing (October 2023), MOHELA's 2022 consolidation as sole PSLF servicer, and multi-state litigation announced in 2024. Complaint volume in 2025 was 10,409, compared to under 1,000 in any year 2020–2022.

The full 25

Every value here traces back to the CFPB search URL in the last column — one paste into the browser reproduces the underlying complaint set. Click any column header to sort. Default order is total complaints since 2020, descending.

| Company |

Total complaints 2020–2025 |

Monetary relief % 2020 |

Monetary relief % 2025 |

Δ (pp) |

Timely response % 2025 |

Verify at CFPB |

Methodology and contamination events

What "monetary relief" means

CFPB's Company response to consumer field is a categorical enum set by the company itself when it closes a complaint. "Closed with monetary relief" means the company gave the consumer money (refund, waiver, credit, settlement). "Closed with non-monetary relief" means an apology, policy change, record correction, or other non-cash remedy. "Closed with explanation" means no relief — the company explained why it declined to act. This page uses CFPB's labels verbatim without redefinition.

What "timely response" means

CFPB gives companies 15 business days to respond substantively to a complaint, with the option to extend to 60 days in limited cases. "Timely" = responded within that window. This is a process metric, not an outcome metric — a company can answer on time and still close without relief.

Contamination events considered when reading this data

- CFPB's 2022 credit-reporting dispute campaign. Starting in 2022, CFPB publicly directed consumers to file credit-report disputes through its portal. Complaint volume against the three credit bureaus rose from ~275K in 2022 to >10M by 2025. The all-25 series in Chart 1 is dominated by this volume shift.

- COVID student-loan payment pause (2020–2023) and October 2023 resumption. The pause suppressed student-loan-servicing complaints; resumption coincides with the volume increase visible in Chart 4.

- MOHELA's 2022 consolidation as sole PSLF servicer. Servicing volume concentrated on one operator whose capacity was sized for the pre-consolidation load.

- 2024 CFPB junk-fees rule. Changed the set of behaviors that became complaint-eligible, affecting the distribution of complaint types for consumer banks and credit-card issuers.

These events affect the composition of the raw numbers. The consumer-bank cluster shown in Chart 2 excludes the three credit bureaus and the student-loan servicer, isolating a subset that is not directly affected by the events listed above.

For the full data pipeline (source definitions, alias resolution, notable-shift auto-detection thresholds, privacy posture), see the main methodology page.